Determining the Amount of Disability Insurance You Require

Disability insurance is a critical aspect of financial protection. It serves as an income replacement measure in case you suffer from an ailment or injury preventing you from performing your regular duties at work. Many people tend to avoid this insurance due to perceived low chances of disability. However, it’s noteworthy that 1 in 4 people experience a disability during their career, with 13% having one that lasts five years or longer. When estimating the coverage you need, several factors come into play including your expenses, other sources of income, and your savings.

Calculating the required disability insurance involves looking into your current spending habits. You would require coverage that can at least cater to your essential expenses. During the period of your disability, some expenses such as commuting costs may decrease, but you might need additional amounts for medical-related transportation. It’s crucial to incorporate these considerations when defining your coverage. After estimating your expenses, identify your potential sources of income during the disability period. These could include retirement savings, returns from a side hustle, and investment incomes. After ascertaining these streams of income, subtract these from your expenses to determine the additional income required for sustaining your lifestyle. This additional income is what you should ideally cover with your long-term disability insurance.

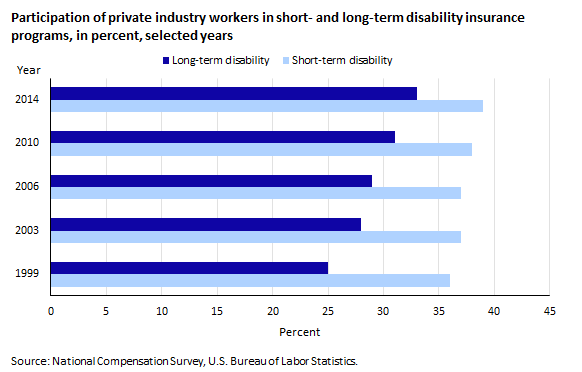

When considering a suitable disability insurance policy, it’s crucial to note that there are two types: short-term and long-term. Short-term policies usually cover a period of 3-6 months whereas long-term insurance covers a longer duration, possibly until retirement. These policies tend to cover between 40-70% of your income.

Expenses and income will vary among individuals, calling for personalized disability insurance coverage. Therefore, you might want to consider enhancing your existing insurance, applying for a supplemental policy, or incorporating specific riders on your policy. The insurance premium costs depend on various factors including your occupation and pre-existing health conditions.

In conclusion, purchasing the ideal disability insurance policy requires adequate planning and a good understanding of your unique financial situation. A financial advisor or insurance professional can provide helpful insights.

On a related note, if you’re undergoing physical limitations and need to claim state benefits such as those offered by the California Employment Development Department, one may need assistance on how to contact EDD or get a hold of services like SDI, PFL, or unemployment benefits in California. To ease this contacting process, visit eddcaller.com for assistance. This resource aids in establishing a connection with a live person at EDD, potentially speeding up your claims process.