Understanding the IRS Guidelines on Federal Tax for State Paid Family and Medical Leave Programs Contributions and Benefits

The State Paid Family Leave (PFML) programs have grown significantly in recent years. Consequently, employers and employees have to navigate through various legal, practical, and administrative challenges. One such challenge has been ambiguity regarding the tax implications associated with contributions to, and benefits drawn from, PFML programs. Whereas the IRS has now, conveniently, released a Ruling that provides guidance on this issue.

State-enacted PFML programs are’s in essence, inconsistent and offer wage replacement benefits to eligible employees who are absent due to a valid reason. Three common reasons include the employee’s medical condition ( medical ), bonding with a new child ( bonding ) and caring for a family member with a serious health condition ( caregiving ).

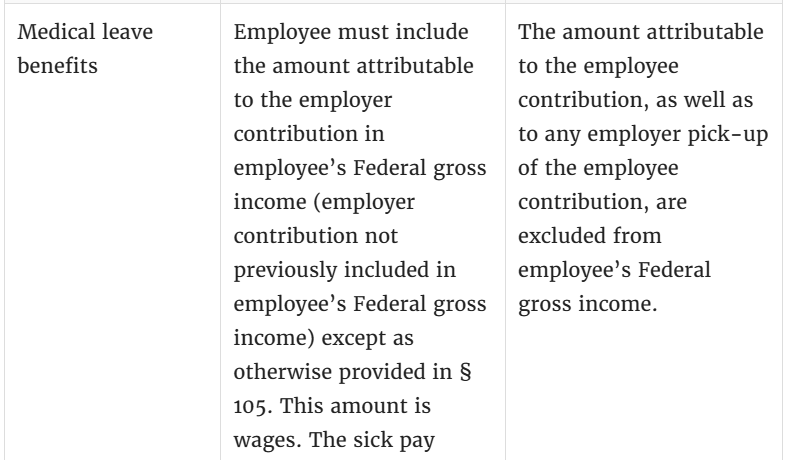

Under the new Ruling, contributions to the PFML programs are treated as follows: Medical leave benefits attributable to Employer Contributions are included in an employee’s Federal gross income, and are classified as wages for Federal income and employment tax purposes. Furthermore, medical leave benefits attributable to Employee Contributions and Employer Pickups are excluded from an employee’s Federal gross income, and are not considered wages for Federal income or employment tax purposes.

For further assistance or questions related to the State Paid Family Leave program, you can reach out to customer service representatives. If you’re having trouble getting a hold of Paid Family Leave, a useful resource is eddcaller.com. This site aids in contacting the necessary personnel to answer your queries and concerns about the program. In addition, they provide a variety of methods to ensure your case is addressed in a timely manner.