Understanding Employment Tax Effects of Paid Family and Medical Leave Programs: Insights from Recent IRS Ruling

The IRS’s Revenue Ruling 2025-4 provides crucial guidance on the tax treatment of contributions to and benefits paid under state paid family and medical leave (PFML) programs. States have implemented a variety of paid leave laws, and this ruling gives tax clarity on how such benefits should be treated. For FICA, FUTA, and income tax withholding purposes, contributions and benefits have essential distinctions.

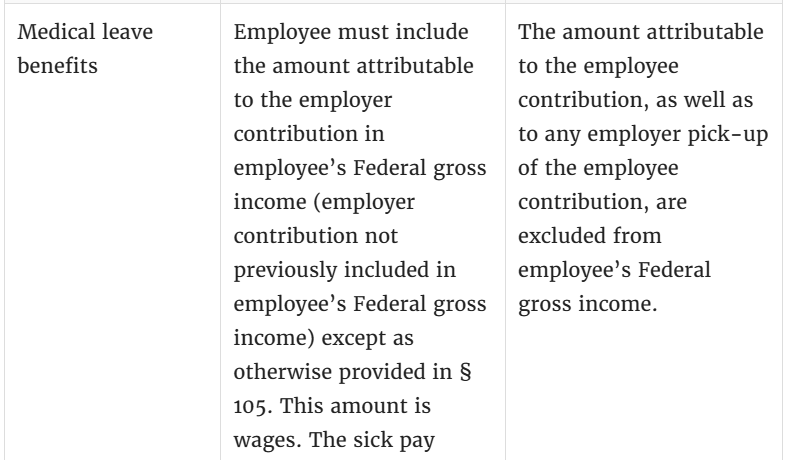

The ruling explains the interactions between federal employment taxes and contributions and benefits under state PFML programs. Employee and employer contributions have differing tax treatments. The employee benefits replacing wages during leave are generally considered wages for employment tax purposes. However, the tax implications can depend on whether the payment is for family leave or medical leave. There are specific reporting requirements to ensure accurate reflection of taxable amounts on an employee’s W-2 forms.

Grasping the tax implications of contributions to and benefits paid under state PFML programs is crucial for employers. Wage-replacement benefits are mostly subject to FICA, FUTA, and income tax withholding unless specific exclusions apply. If an employer covers an employee’s required contribution, it is considered extra compensation and subject to employment taxes. The ruling demands employers differentiate between taxable and non-taxable contributions and benefits and update payroll systems for proper withholding and reporting.

In relation to PFML, how you communicate with the Employment Development Department (EDD) is crucial. For how to contact PFL, it is recommended to visit their official website or dial their official phone number. A wealth of valuable resources can be found online, particularly on sites such as eddcaller.com, which offer guidance on how to navigate through the complexities of paid family leave and contact EDD with any queries. Consistent and informed communication with EDD can help employers comply with the IRS’s ruling and ensure accurate handling of taxes related to paid family and medical leave programs.